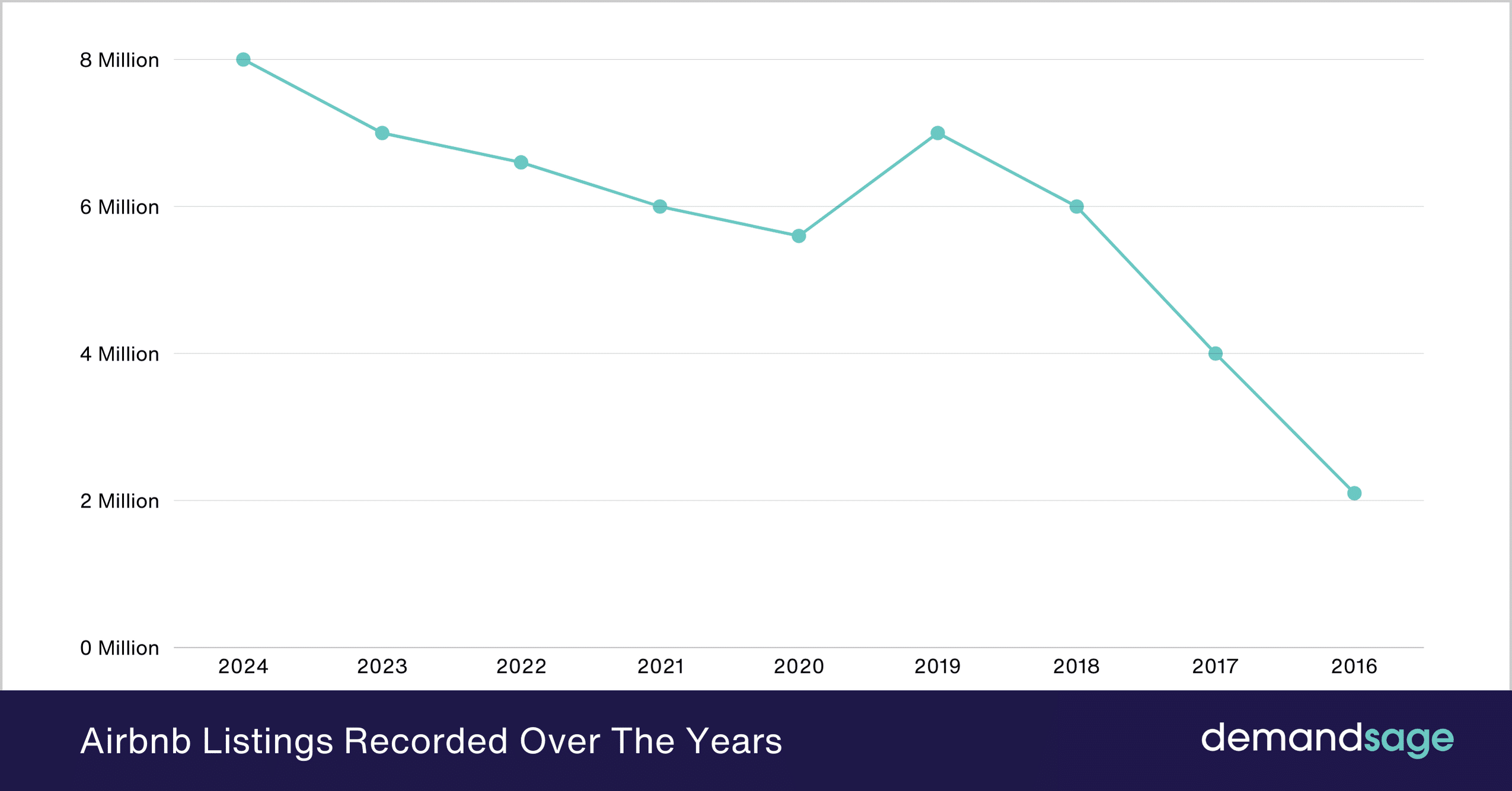

Airbnb occupancy: 2026 forecast

Airbnb markets are stabilizing after the post-pandemic rush. Global occupancy rates for early 2025 are sitting between 65% and 75%. While the US and Europe have cooled off since 2023, Southeast Asia is picking up speed. Looking toward 2026, we have to account for tighter regulations and shifting travel habits rather than assuming the current growth just continues indefinitely.

There is no such thing as a universal occupancy rate. A Bali villa operates on a different planet than a spare room in a suburban basement. Data from AirDNA or Rabbu often conflicts because they use different math, so I take broad averages with a grain of salt.

Looking ahead to 2026, I anticipate a more segmented market. Mature markets will likely see modest growth or stagnation, dependent on local economic conditions and regulatory changes. Emerging markets, particularly those benefiting from increased tourism infrastructure and favorable policies, present the most promising opportunities. However, these opportunities aren’t without risk; investors must carefully assess the political and economic stability of these regions. The key to success will be data-driven decision making and a deep understanding of local market dynamics.

Occupancy rates in major cities

Analyzing specific cities reveals a nuanced picture of Airbnb occupancy. Here’s a look at several major markets, based on data from AirDNA and Airbtics as of late 2024/early 2025, along with projections for 2026.

New York City: Currently around 68% occupancy, severely impacted by stringent regulations. I project this to remain around 65% in 2026, with limited recovery unless regulations are eased. The city’s high cost of living and limited supply of legal short-term rentals will continue to constrain growth.

Paris: Occupancy sits at approximately 79%, benefiting from consistent tourism demand. The 2024 Olympics will provide a temporary boost, but I expect occupancy to settle around 76% in 2026 as the effect fades. Increasing competition from hotels and potential new regulations related to the Games are factors to watch.

London: Occupancy is around 72%, facing challenges from rising living costs and Brexit-related uncertainties. A projected 70% occupancy in 2026 reflects a conservative outlook, factoring in potential economic slowdowns. However, London’s status as a global hub will continue to attract visitors.

Miami: Currently boasting an impressive 85% occupancy, driven by strong domestic and international demand. I anticipate this to moderate slightly to 82% in 2026, as new supply enters the market and economic conditions normalize. The city’s appeal as a leisure destination remains strong.

Tokyo: Occupancy is around 75%, steadily recovering from the pandemic. The ongoing influx of tourists and a favorable exchange rate are driving growth. A projected 78% occupancy in 2026 is realistic, assuming continued economic stability and relaxed travel restrictions.

Bangkok: Experiencing high demand with 80% occupancy, driven by affordable prices and a vibrant tourism scene. I forecast 83% occupancy in 2026, fueled by increasing tourism from China and other Asian countries.

Barcelona: Occupancy at 77%, but heavily impacted by local regulations limiting short-term rentals. Projections for 2026 suggest a slight decline to 74% if these restrictions remain in place. Hosts are adapting by offering longer-term rentals or exploring alternative platforms.

- New York City: 65% projected for 2026

- Paris: 79% (2025), 76% (2026)

- London: 72% (2025), 70% (2026)

- Miami: 85% (2025), 82% (2026)

- Tokyo: 75% (2025), 78% (2026)

- Bangkok: 80% (2025), 83% (2026)

- Barcelona: 77% (2025), 74% (2026)

Airbnb Occupancy Rates: 2024/2025 vs. 2026 Projections & Risk Assessment

| City | 2024/2025 Rate (%) | 2026 Projected Rate (%) | Key Factors Influencing Projection | Risk |

|---|---|---|---|---|

| Nashville, TN | 68.7% | 71.5% | Continued tourism growth, expansion of event hosting, relatively favorable short-term rental regulations. | Potential for increased regulation targeting non-owner occupied rentals. |

| Miami, FL | 75.3% | 78.2% | Strong international tourism, consistent demand for luxury rentals, limited new construction in prime areas. | Hurricane season disruption, potential oversupply of new units if construction accelerates. |

| Orlando, FL | 72.1% | 74.8% | Theme park attendance remaining high, increasing demand for family-sized accommodations, expansion of entertainment offerings. | Economic downturn impacting travel budgets, potential for increased competition from new resorts. |

| New Orleans, LA | 65.9% | 68.1% | Resurgence of tourism following pandemic recovery, consistent event calendar, unique cultural appeal. | Potential for stricter regulations on short-term rentals in historic districts, impact of severe weather events. |

| Austin, TX | 62.5% | 65.0% | Continued population growth attracting corporate and leisure travelers, strong tech industry presence, vibrant music scene. | Increasing property taxes and insurance costs, potential for stricter enforcement of existing regulations. |

| Savannah, GA | 70.4% | 73.0% | Growing popularity as a leisure destination, historic charm, relatively affordable compared to other coastal cities. | Potential for increased congestion and strain on infrastructure, leading to regulatory changes. |

| Phoenix, AZ | 64.3% | 66.8% | Warm weather attracting 'snowbirds' and leisure travelers, increasing popularity for outdoor activities, relatively lower cost of living. | Water scarcity concerns potentially impacting tourism, extreme heat during summer months. |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

How property types compare

The performance of different property types varies considerably. Entire homes consistently achieve the highest occupancy rates, generally between 70-85% in popular markets. This is driven by demand from families and groups seeking privacy and space. Private rooms, while offering lower price points, typically see occupancy rates in the 50-65% range. They are more sensitive to economic fluctuations and competition from hotels.

Hotel rooms listed on Airbnb—a relatively recent phenomenon—are a mixed bag. Occupancy depends heavily on the hotel's location, branding, and pricing strategy. They often struggle to compete with dedicated Airbnb listings, but can be successful in areas with limited short-term rental supply. Multi-unit listings, where a single owner manages multiple properties, are becoming increasingly prevalent. These listings can benefit from economies of scale and professional management, but also face greater scrutiny from regulators.

Looking ahead to 2026, I expect entire homes to remain dominant, but private rooms might see a resurgence as travel budgets tighten. The increasing popularity of 'bleisure' travel – blending business and leisure – could also boost demand for well-equipped entire homes with workspaces. However, the regulatory landscape will continue to play a significant role; restrictions on entire-home rentals could shift demand towards private rooms and hotels.

Seasonality and Peak Demand Periods

Occupancy rates are rarely consistent throughout the year. Peak seasons, driven by holidays, school breaks, and major events, consistently generate the highest demand. For example, coastal destinations experience a surge in occupancy during the summer months, while ski resorts peak during the winter. Major cities see increased demand during conferences and festivals.

However, these traditional patterns are evolving. The rise of remote work has blurred the lines between peak and off-peak seasons, leading to more consistent demand throughout the year. Shoulder seasons—the periods between peak and off-peak—are becoming increasingly important as travelers seek to avoid crowds and take advantage of lower prices. Understanding micro-seasonality—specific events or festivals that drive localized demand—is crucial for maximizing revenue.

Climate change and extreme weather events are also impacting seasonality. Unpredictable weather patterns can disrupt travel plans and shift demand to different destinations. Hosts need to be prepared for these disruptions and adjust their pricing and marketing strategies accordingly. For example, areas prone to hurricanes may experience a decline in occupancy during hurricane season.

The impact of local laws

Short-term rental regulations are having a profound impact on occupancy rates in many cities. New York City, with its strict rules requiring hosts to be present during stays and limiting rental durations, has seen a significant decline in Airbnb listings and occupancy. Barcelona and Amsterdam have also implemented stringent regulations, resulting in reduced supply and increased enforcement.

Cities with more lenient regulations, such as Miami and Lisbon, have generally experienced higher occupancy rates and continued growth. However, even these cities are facing increasing pressure from local residents concerned about the impact of short-term rentals on housing affordability and neighborhood character. The regulatory landscape is constantly evolving, making it difficult for hosts and investors to predict the future.

Hosts are adapting to these regulations in various ways, including switching to longer-term rentals, operating through property management companies, or exploring alternative platforms. However, these strategies often come with trade-offs, such as lower revenue or increased costs. The outlook for 2026 is uncertain; further regulatory changes are likely, and hosts will need to remain flexible and adaptable.

- New York City: Strict regulations, significant occupancy decline.

- Barcelona & Amsterdam: Stringent rules, reduced supply.

- Miami & Lisbon: Lenient regulations, continued growth.

Cities with STR Regulations

- New York City, NY - Operates a strict registration system for short-term rentals, requiring hosts to be present during the stay and limiting rentals to a single unit. Local Law 18 significantly restricts unregistered listings.

- Paris, France - Requires hosts to register with the city and obtain a registration number, limiting the number of days a property can be rented annually (maximum 120 days, with exceptions).

- Barcelona, Spain - Imposes a moratorium on new tourist licenses in the city center, and requires all rentals to be registered with the Registre de Turisme de Catalunya.

- Amsterdam, Netherlands - Limits the number of days a property can be rented out to tourists (maximum 60 days per year) and requires a permit for short-term rentals. Enforcement is actively monitored.

- Santa Monica, California - Prohibits short-term rentals of entire homes for less than 30 days. Home-sharing is permitted only if the host is present during the rental period.

- Berlin, Germany - Generally prohibits short-term rentals of entire apartments without a permit. A permit is required if the rental is expected to disrupt the local housing market.

- Florence, Italy - Requires registration of short-term rental properties with the Comune di Firenze and imposes limits on rental periods and guest numbers.

Investment Hotspots: Standout Opportunities

Based on the data analysis, several cities present particularly attractive investment opportunities for short-term rentals in 2026. These aren't necessarily the most popular tourist destinations, but rather markets with a combination of strong occupancy rates, favorable regulations, and potential for growth.

Medellin, Colombia: Offers a low cost of living, a growing tourism industry, and relatively lenient regulations. Occupancy rates are consistently high, and the city is attracting an increasing number of digital nomads and remote workers. Investors should focus on properties in popular neighborhoods like El Poblado and Laureles.

Lisbon, Portugal: Continues to be a popular destination for tourists and expats, with a vibrant culture and affordable prices. While regulations are becoming stricter, the overall outlook remains positive. Look for properties in historic neighborhoods like Alfama and Bairro Alto.

Mexico City, Mexico: A rapidly growing tourism market with a rich history and diverse culture. Occupancy rates are high, and the city is attracting a new generation of travelers. Focus on properties in central neighborhoods like Roma Norte and Condesa. Investors should be aware of potential safety concerns and ensure properties are well-maintained.

These cities share several key characteristics: a growing tourism industry, relatively affordable prices, and a favorable regulatory environment. However, investors should conduct thorough due diligence and consult with local experts before making any investment decisions. Specific criteria to consider include property location, condition, and potential rental income.

No comments yet. Be the first to share your thoughts!