Historical trends in Olympic host cities

Major sporting events, and the Olympics in particular, consistently cause ripples in the short-term rental market. The pattern isn’t always simple, but a clear correlation emerges when examining past host cities. Looking back at London 2012, Rio 2016, and Tokyo 2020 – even with the pandemic complicating the latter – we see predictable, though varying, shifts in Airbnb occupancy rates and average daily rates (ADR).

AirDNA data for London 2012 demonstrates a significant spike in occupancy during the games themselves, peaking at around 85% for properties within a 5km radius of the Olympic Park. This was a roughly 40% increase compared to the same period in the previous year. However, the surge was relatively short-lived, with occupancy returning to pre-Olympic levels within three months. Rio 2016 saw a similar pattern, but the recovery was slower, likely due to political and economic instability in Brazil at the time.

Tokyo 2020, held in 2021, presented a unique case. Occupancy rates were initially suppressed by travel restrictions, but saw a notable increase as the games approached and restrictions eased. While the spike wasn't as dramatic as in London or Rio, it was still significant – around a 30% increase in occupancy within central Tokyo. The key takeaway from these events is that the magnitude and duration of the impact are heavily influenced by local economic conditions, political stability, and pre-existing tourism infrastructure.

Daily rates climb when demand outstrips supply, but these spikes rarely last. I've seen hosts struggle by holding onto Olympic-level pricing for too long. The data shows that dropping back to market rates quickly is more effective than watching a calendar stay empty at inflated prices.

What we learned from Paris 2024

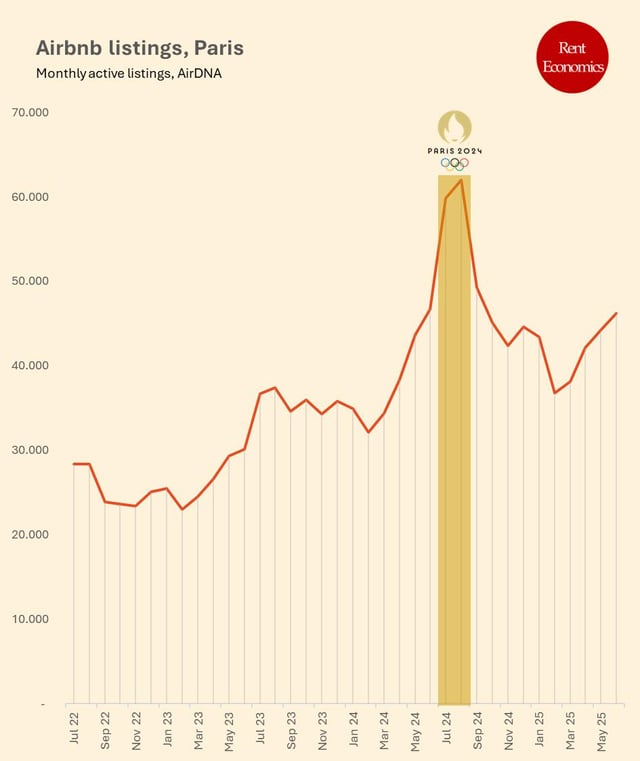

The Paris 2024 Olympics offer a very recent and valuable data point for understanding the impact of these events on the Airbnb market. Preliminary data from AirDNA shows a substantial increase in demand starting in the spring of 2024, with occupancy rates rising steadily in the months leading up to the games. Airbtics data corroborates this, showing a peak occupancy rate of approximately 88% across Paris during the Olympic period (July 26 - August 11).

Looking at RevPAR, the picture is even more striking. According to AirDNA, RevPAR in Paris increased by over 150% during the Olympics compared to the same period in 2023. This was driven by both higher occupancy and significantly higher ADR, which saw an average increase of 80%. However, the data also reveals significant variations between different neighborhoods. Central arrondissements, such as the 1st, 4th, and 6th, experienced the largest increases in both occupancy and ADR.

Interestingly, the initial post-Olympic dip appears to have been less severe than in previous host cities. While occupancy rates did decline in the weeks following the games, they remained above pre-Olympic levels. This suggests that the Olympics generated a sustained level of interest in Paris as a tourist destination, potentially due to increased media coverage and positive word-of-mouth. It's too early to determine if this effect will be long-lasting, but it’s a promising sign for hosts.

A notable trend observed during Paris 2024 was the increased demand for longer stays. According to Airbtics, the average length of stay increased by approximately 20% during the Olympics, suggesting that visitors were planning extended trips to coincide with the games. This is a positive development for hosts, as longer stays typically result in higher revenue and lower turnover costs.

- Paris 2024 occupancy peaked at 88% according to Airbtics.

- AirDNA reported a RevPAR increase of over 150%.

- ADR Increase (Paris 2024): 80% (AirDNA)

- Average Length of Stay Increase: 20% (Airbtics)

Paris Airbnb Performance: Q1 2024 vs. Olympic Period vs. Post-Olympic Period

| Metric | Q1 2024 | July-August 2024 (Olympics) | September-October 2024 | Percentage Change (Olympics vs. Q1 2024) | Percentage Change (Post-Olympics vs. Olympics) |

|---|---|---|---|---|---|

| Occupancy Rate | 68.2% | 89.5% | 62.1% | +31.2% | -30.6% |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

Milan-Cortina 2026: Market Characteristics

Milan and Cortina d'Ampezzo present distinct Airbnb markets. Milan, a major economic and fashion hub, already has a well-established short-term rental scene, catering to business travelers, tourists, and students. Cortina d’Ampezzo, in contrast, is a smaller, more seasonal resort town in the Dolomites, primarily attracting skiers and hikers. Understanding these differences is crucial for predicting the impact of the 2026 Olympics.

Milan has over 17,000 listings on Rabbu, ranging from studios to villas. Occupancy stays between 65% and 70% most of the year, though it spikes during fashion week. Cortina d'Ampezzo is smaller, with 3,000 listings, and its market is strictly seasonal—busy in the winter and quiet in the summer.

The Milanese market is relatively competitive, with a mix of professional property managers and individual hosts. Cortina d'Ampezzo, however, is dominated by individual hosts, many of whom own second homes in the area. This difference in market structure could influence pricing strategies and the overall response to the Olympics. The existing tourism infrastructure in both locations is well-developed, but the Olympics are expected to bring a significant influx of visitors, requiring further investment in transportation and accommodation.

The types of travelers typically drawn to Milan and Cortina d'Ampezzo also differ. Milan attracts a more diverse demographic, while Cortina d'Ampezzo primarily caters to affluent tourists seeking outdoor activities. The Olympics are likely to broaden the appeal of both locations, attracting a wider range of visitors and potentially driving long-term growth in the short-term rental market.

The reality of the post-Olympic slump

Based on historical data and the unique characteristics of the Milan-Cortina market, predicting the post-Olympic dip is challenging, but we can assess likely scenarios. Past Olympic host cities have typically experienced a decline in occupancy rates in the months following the games, ranging from 15% to 40%, depending on local conditions. I anticipate Milan will see a drop in the 20-30% range, while Cortina d’Ampezzo could experience a more significant decline, potentially exceeding 35%, due to its stronger seasonal dependence.

Several factors could mitigate the severity of the dip. The extent to which the Olympics generate sustained interest in the region is paramount. Effective marketing and promotion by local tourism boards can play a crucial role in maintaining momentum. Focusing on attracting visitors during the shoulder seasons – spring and fall – could help to fill the gap left by the departing Olympic crowds. This requires targeted marketing campaigns highlighting the region’s attractions beyond the winter sports season.

The potential for a "shoulder season" effect is higher in Cortina d'Ampezzo, as the Olympics could raise awareness of the Dolomites as a year-round destination. Milan, with its established tourism infrastructure and diverse attractions, is better positioned to weather the post-Olympic dip. However, hosts in both locations should be prepared to adjust their pricing strategies and offer incentives to attract guests.

The global economy is the wild card here. A recession would make the post-event slump much deeper. I'm not sure exactly how far the numbers will fall, but if you own a rental there, you should prepare for a quiet 2027.

Projected Airbnb Occupancy Rates: Milan & Cortina d'Ampezzo (Post-2026 Olympics)

Data: AI-generated estimate for illustration

When to buy in Milan and Cortina

For real estate investors, timing is critical when considering properties in Milan or Cortina d'Ampezzo. Purchasing before the Olympics presents the potential for capital appreciation, but also carries the risk of overpaying due to inflated prices. The market has likely already begun to factor in the Olympic effect, so gains may be limited. Thorough due diligence, including a detailed analysis of local regulations and potential rental income, is essential.

Investing during the games is generally not advisable. Prices are at their peak, and the opportunity to generate immediate rental income is limited. However, it could be an option for investors seeking a quick flip, assuming they can accurately predict the post-Olympic market correction. This is a high-risk strategy that requires significant expertise and a deep understanding of the local market.

Purchasing after the Olympics, once the initial post-event dip has occurred, may offer the most attractive investment opportunity. Prices are likely to be lower, and there’s potential to capitalize on the increased awareness of the region generated by the games. However, investors need to be prepared to wait for the market to recover and ensure the property is well-positioned to attract guests. It's important to understand local restrictions on short-term rentals before making any investment.

Regardless of when you invest, remember that short-term rental regulations can change. Both Milan and Cortina d'Ampezzo have specific rules governing short-term rentals, and these rules could be amended in the future. It's essential to stay informed about any changes and ensure your property complies with all applicable regulations. Consulting with a local real estate attorney is highly recommended.

Beyond Occupancy: ADR & Revenue Shifts

While occupancy rates are a key metric, they don’t tell the whole story. Average Daily Rate (ADR) and overall revenue are equally important. The Olympics typically lead to a significant increase in ADR, but maintaining these higher prices after the games is a challenge. The extent to which hosts can do so depends on the sustained demand for the region and the level of competition.

Data from past Olympic host cities suggests that ADR typically returns to pre-Olympic levels within six to twelve months. However, the Olympics can also lead to a long-term shift in pricing power for hosts, particularly in desirable locations. If the games successfully position the region as a premier tourist destination, hosts may be able to command higher prices year-round.

Increased competition is another factor to consider. The influx of new listings in the lead-up to the Olympics can put downward pressure on prices. Hosts need to differentiate their properties by offering unique amenities, exceptional service, and competitive pricing. Investing in property upgrades and professional photography can also help to attract guests.

AirDNA and Airbtics data will be crucial for monitoring ADR trends in Milan and Cortina d'Ampezzo in the months following the Olympics. Hosts should be prepared to adjust their pricing strategies based on market conditions and competitor activity. A flexible pricing approach is essential for maximizing revenue in a dynamic market.

No comments yet. Be the first to share your thoughts!